Get Separate Bank Accounts

Everyone Gets an Account

Whether you run a portfolio of long-term rentals or operate a few Airbnbs, your real estate portfolio is a real business. You should absolutely treat it like one!

One of the single best things you can do to get organized and drive operating leverage is to open a separate bank account for each rental property.

The process typically isn’t complicated or expensive, and the benefits compound over time. Here’s why separate accounts matter and how to set them up correctly.

Reason #1: Effortless Income & Expense Tracking

Peace of mind and simplicity are just two compelling reasons to maintain separate bank accounts for rental properties.

The problem with commingling funds:

Imagine using one personal checking account for everything:

- Your paycheck deposits

- Grocery shopping

- Rent from Property A

- Maintenance expenses for Property B

- Airbnb payouts from Property C

- Your mortgage payment(s)

- HOA fees for Property A

- Guest refund for Property C

Come tax time, you’re staring at hundreds of transactions trying to remember: “Was that $347 Home Depot expense for my house or the rental? Which rental?” That’s a mess, that only worsens with each new property acquisition.

The solution:

One bank account per property. Every deposit and expense for Property A flows through Account A. Property B uses Account B exclusively. Your finance stack suddenly becomes dramatically more organized and can be automated much more easily when there is a 1:1 relationship between bank accounts and properties.

Modern Accounting Integration

If you use accounting software like QuickBooks, FreshBooks, or Xero, you can usually connect bank accounts directly to import transactions automatically. This is where separate accounts really shine. Airbnb and the other OTA platforms also now offer the ability to direct payouts into different bank accounts for each property, which can save a ton of time and hassle on the bookkeeping side of things.

There’s typically no extra cost, beyond your time, to set up multiple accounts at a single bank or credit union.

With one combined account: All transactions import as a jumbled mess. You manually categorize every line item—”Property A expense,” “Property B income,” “personal expense (ignore),” etc.

With separate accounts: Connect Account A directly to Property A in your accounting system. Connect Account B to Property B. While transactions can often auto-categorize upon import, we think it’s still important to review monthly to make minor adjustments and get a feel for how your assets are performing.

In our estimation, automations like this can regularly save 2-3 hours per month per property. If you own three rentals, that’s 6-9 hours you’re not spending on bookkeeping every month.

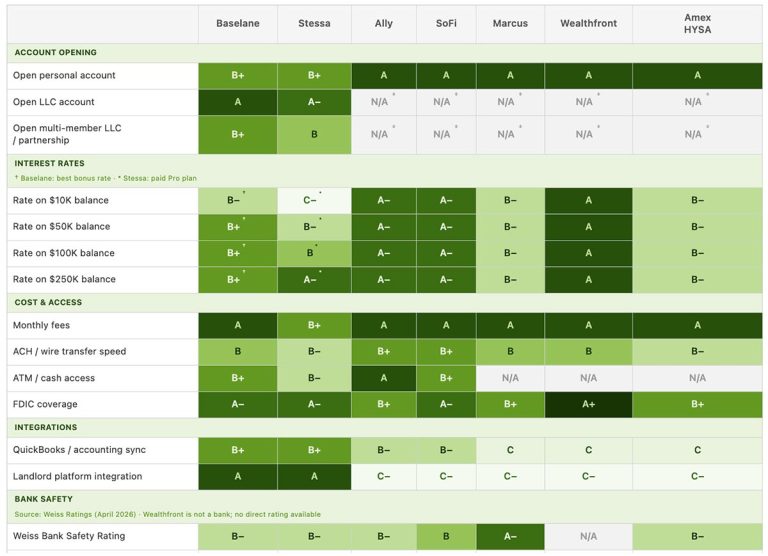

Reason #2: High-Yield Interest Actually Matters Now

In 2020, when I first published this article, high-yield savings accounts (HYSAs) paid around 1.5-2.0%. Traditional bank savings accounts paid basically nothing—maybe 0.05-0.10%.

Fast forward to 2026: Online banks are now paying 4.0-4.5% APY on high-yield savings accounts. Traditional brick-and-mortar banks? Still around 0.39% on average.

That’s a 10x difference.

Real Numbers

Let’s say your average rental account balance is $8,000 (security deposits, reserves for maintenance, accumulated rent before paying the mortgage, etc.).

Traditional savings account (0.39% APY):

- Annual interest: $31

- After 5 years: $157 total interest earned

High-yield savings account (4.25% APY):

- Annual interest: $340

- After 5 years: $1,847 total interest earned

Difference: $1,690 in your pocket instead of the bank’s pocket. Per property.

If you have three rental properties with similar balances, that’s over $5,000 in found money over five years—just for taking the time to move into higher-yielding accounts.

Where to Open High-Yield Accounts (2026)

Some top online banks for rental property accounts include:

- Ally Bank – 4.25% APY, no minimums, excellent mobile app

- Marcus by Goldman Sachs – 4.20% APY, no fees

- American Express Personal Savings – 4.20% APY, easy integration if you have Amex business cards

- Capital One 360 – 4.10% APY, good if you want both checking and savings

- Discover Bank – 4.00% APY, established online bank

These online accounts typically offer:

- No monthly fees

- No minimum balance requirements

- FDIC insured up to $250,000 (or more)

- Easy electronic transfers

- Mobile deposit for checks

Pro tip: Have rental income deposited directly into a high-yield savings account. Then set up automatic transfers to sweep funds into a linked checking account as needed to cover your mortgage and expenses.

Reason #3: Operating As an LLC

If you’ve set up an LLC for your rental properties (you may want to seriously consider it if you haven’t already—see our guide on LLCs for rental properties), you need to operate it like an actual business to receive the protective benefits. That typically means you want to open business bank accounts in the LLC’s name.

Why This May Matter Legally

Courts have repeatedly ruled that simply forming an LLC isn’t enough to protect your personal assets. If you want to increase the chances that your LLC can shield you from actual lawsuits, you should, at a minimum:

- Maintain separate finances – Business money flows through business accounts

- Use the LLC name consistently – Rent checks made out to “ABC Properties LLC,” not to you personally

- Avoid commingling – Don’t pay personal expenses from LLC accounts (or vice versa)

- Keep proper records – Bank statements showing clear business-only activity

If you fail to do this, opposing counsel will likely argue you’re not really operating as a business and that the LLC is a sham or a front. Courts call this “piercing the corporate veil,” and when it happens, your personal assets can become fair game in a lawsuit.

Setting Up Business Accounts

What you usually need (requirement vary):

- LLC formation documents from your state

- EIN (Employer Identification Number) from the IRS (free, takes 10 minutes online)

- Operating agreement (even if you’re a single-member LLC)

- Personal ID

Where to open business accounts:

Many online banks (Ally, Marcus, etc.) don’t offer business accounts. You’ll likely want to start with:

- Local credit union – Often the best rates and lowest fees for small business accounts

- Chase Business Banking – Convenient if you travel, decent online tools

- Bank of America Business Advantage – Good integration if you already bank there personally

- U.S. Bank – Competitive small business checking options

Monthly fees: Expect $10-15/month unless you maintain minimum balances (usually $1,500-5,000). Some credit unions waive fees entirely for small businesses.

Is it worth the fee? Absolutely. $120-180/year in fees is a small price for the organizational benefits, flexibility, and potential legal protections that may come with maintaining separate business bank accounts for each property (or portfolio of properties).

Reason #4: Dedicated Credit Cards Complete the System

Once you have separate bank accounts, the next logical step is to open dedicated business credit cards for each property (or at least one per LLC if multiple properties share an LLC).

Benefits of Dedicated Credit Cards

1. Automatic categorization: All rental expenses can be imported into your bookkeeping solution via a 1:1 relationship for easy tagging and categorization. You’ll no longer have to wonder, “was that trip to the hardware store for 123 Oak St or 789 Cedar Dr?”

2. Cash back on business expenses: Business cards often offer 2% cash back on everyday purchases. If you put $15,000 in annual rental expenses on a 2% card, that’s $300 back per year.

3. Better fraud protection: Business cards often have stronger fraud protection than personal cards. If your card number is compromised or there’s fraudulent activity, you may have better protection and more recourse than you would with a personal credit card.

4. Builds business credit: Helps establish credit history for your LLC, which could in turn make it easier to get business loans in the future.

5. Simplifies tax time: Having separate credit card statements for each property or portfolio can really accelerate your tax readiness. Those statements show clear lists of potential tax deductions, which can feed into your Schedule E once properly categorized.

Setup Strategy

Auto-pay from your business checking account: Set the credit card to auto-pay in full each month from the property’s business checking account. This creates a clean loop:

- Rental income → Business checking account

- Expenses → Business credit card

- Auto-pay → Credit card paid from business checking

- End of month → Clear paper trail for taxes

Recommended business cards for rental properties (2026):

- Chase Ink Business Cash – 5% back on utilities, internet, phone (up to $25K/year), 2% on gas stations

- American Express Blue Business Cash – 2% cash back on all purchases (up to $50K/year)

- Capital One Spark Cash – Flat 2% on everything, simple structure

- Bank of America Business Advantage Cash Rewards – 3% back on category of your choice

Annual fees: Most of these have $0-95 annual fees. The cash back usually more than covers the fee if you are diligent about making sure all rental expenses go through the card(s).

Reason #5: Simplified Tax Preparation

This is where everything comes together.

With separate accounts and dedicated credit cards:

- January rolls around

- Log into your business checking account

- Download the annual statement (or let your accountant access it directly)

- Download the business credit card statement

- Cross-check against your bookkeeping reports

Compare this to the alternative:

Commingled personal/business accounts mean:

- Manually reviewing 12 months of statements

- Highlighting rental income and rental expenses

- Personal transactions

- Creating a spreadsheet to summarize everything

- Praying you didn’t miss anything or double-count

The first approach takes 30-60 minutes. The second approach can take 4-8 hours, per property. That’s a big difference.

Bonus: Mid-Year Financial Check-Ins

Separate bank accounts can also make it trivial to check how your properties are performing throughout the year.

Questions you can answer in 60 seconds:

- Is Property A cash-flowing this year?

- How much have I spent on maintenance at Property B?

- What’s my effective vacancy rate at Property C?

- Am I on track for my income projections?

With commingled accounts, answering these questions requires reconstructing months of data. With separate accounts that are tied to an automated bookkeeping solution, you just log in monthly, do a bit of housekeeping and run your reports!

How to Set This Up (Step-by-Step)

For Each Rental Property:

Step 1: Open a high-yield savings account (Ally, Marcus, etc.)

- This is where rental income lands first

- Earns 4%+ interest on your reserves and float

- No fees, easy to set up online

Step 2: Open a business checking account (if using an LLC)

- Need: LLC documents + EIN + ID

- Use local credit union or national bank

- Set up auto-transfer from savings to checking to cover monthly expenses

Step 3: Get a business credit card

- Apply through same bank as checking (easier) or get standalone

- Set up auto-pay from business checking account

- Use this card exclusively for rental property expenses

Step 4: Update payment collection

- Your tenants direct-deposit into high-yield savings (or use an online rent collection service)

- For Airbnb/VRBO: Update payout bank account(s) in platform settings

- For long-term tenants: Provide new account for ACH/check deposits

Step 5: Connect to accounting software (optional but recommended)

- QuickBooks, FreshBooks, or Xero

- Link all three accounts (savings, checking, credit card)

- Set up automatic transaction import

- Review monthly, categorize anything unusual

Time investment: Probably 2-3 hours to set up each property initially. After that, 30-60 minutes per month for oversight.

FAQ

Yes. Even with one rental, separating business from personal finances can make tax prep easier, protect your LLC (if you have one), and earn you higher interest. The benefits will typically outweigh the minimal setup hassle.

You can use one set of accounts for the LLC, but consider sub-accounts or clear labeling in your accounting software to track each property’s performance separately. Some banks offer multiple checking accounts under one business relationship with no extra fees.

If you’re operating as a sole proprietor without an LLC, personal accounts might be fine (though you still want them separate from your everyday accounts). If you have an LLC, use business accounts in the LLC’s name to help maintain legal protection.

Venmo and PayPal or more consumer-oriented services and we generally don’t recommend using them for rent collection. Zelle is a different story but has its own pros and cons. Either way, we don’t recommend leaving money sitting in PayPal or Venmo—it’s typically not FDIC insured and doesn’t earn meaningful interest. Transfer those funds into your high-yield account(s) as soon as possible.

Make the Investment Now

While it takes some extra effort up front, once you have separate bank accounts for each rental property or Airbnb investment, you’ll likely find that precious time is freed up for more lucrative pursuits. You won’t have to juggle expenses between accounts and reconcile your personal and business spend across different properties each month. Instead, you’ll be able to put most of it on auto-pilot from day one and then run a few simple reports when tax time rolls around.