Get Better Landlord Insurance Quotes, Fast

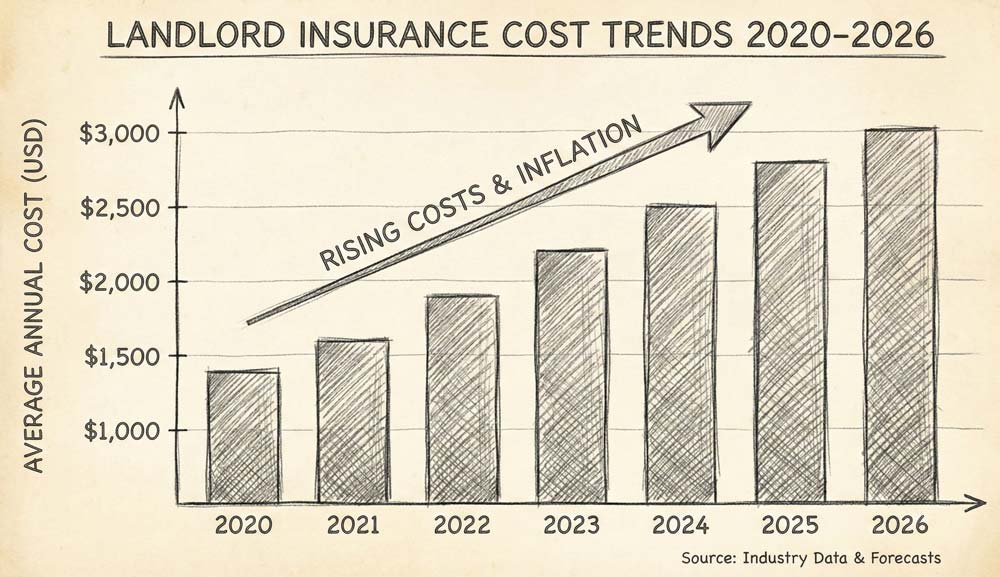

Landlord insurance premiums jumped 5-15% in 2026 for many investors, even those with zero claims. And some markets are seeing 25-50% increases year-over-year. Many Florida landlords are paying $2,200-$4,600 annually. Some California investors have faced 7-10% rate hikes on top of already elevated premiums. North Carolina insurers just filed for a 68% dwelling policy increase over two years.

It’s clearly in your interest to get multiple insurance quotes on a regular basis, maybe even every 6 months.

And yet most landlords are still calling around one carrier at a time, answering the same questions over and over, wasting hours of their precious time to hopefully save a few hundred bucks—if they bother shopping at all.

That’s what I did for years until I found a better way. Now I let the insurance companies who want my business do all the hard work. I sit back and watch golf on TV while Allstate, GEICO, and State Farm sharpen their pencils.

Here’s how you can implement a simple Excel-based system to generate competitive quotes and save money on rental property insurance.

Why Landlord Insurance Costs Keep Rising

Before we get into the solution, let’s understand what you’re up against in 2026:

The main drivers:

- Hailstorms and roof claims – The frequency and severity of actual storms has increased, plus aggressive roofers are now “storm chasing” and knocking on doors once the weather clears to look for work.

- Climate risk – Wildfires in California, hurricanes in Florida, and severe storms in Texas are all pushing premiums higher.

- Construction costs – Materials and labor are still up 5%+ year-over-year, even as general inflation has cooled.

- Reinsurance rates – Insurance companies’ own insurance costs have spiked, and some of this cost increase is being passed through to landlords.

- Up to 70% underinsured – Many existing policies had premiums built on outdated replacement cost estimates, which resulted in bigger losses for insurers when claims hit. Insurers are now moving to reconcile this disconnect through increased premiums.

The national picture:

- Average landlord insurance: $1,516/year ($126/month)

- Typical range: $800-$3,000/year for single-family rentals

- May be 10-25% more expensive than comparable homeowners insurance

- Budget for 10% renewal increases in 2026 even with clean claims history

Key take-away: No one owns a perfectly “average” rental property, so your mileage will of course vary. But regardless, shopping around isn’t optional anymore. It’s a business necessity.

What Drives Your Premium (And What You Can’t Change)

Your landlord insurance costs are primarily determined by the insurers assessment of risks and the dwelling coverage amount—basically, how much it would cost to rebuild your property from the ground up. But several other factors play a major role:

Factors You Can’t Change:

- Location – Flood plains, wildfire zones, hurricane paths, high crime areas

- Age of property – Older buildings = higher premiums

- Square footage – Bigger properties cost more to insure

- Construction type – Frame construction costs more than brick/masonry

- Number of units – More doors = more liability exposure

- Local replacement costs – Labor and materials vary dramatically by market

Factors You Can Influence:

- Deductible amount – Higher deductibles = lower premiums

- Liability coverage limits – Balance protection needs with cost

- Loss of rent coverage – Match to your actual rental income

- Security features – Alarm systems, monitoring, smart locks

- Claims history – Avoid small claims; self-insure minor losses

Pro tip from experienced investors: As your portfolio grows, you may want to consider shifting to higher deductibles ($2,500-$10,000) and/or increasing your liability coverage ($2M-$5M). You’ll often lower your total annual premiums while getting better catastrophic protection. Just make sure you have reserves to cover those deductibles when needed.

That game can only take you so far though, since lenders generally have a minimum requirement for dwelling coverage and sometimes also enforce a maximum deductible. It can also be a risky strategy. In the event of a significant loss, you might find yourself without enough proceeds to rebuild. We advise you to carefully assess your own risk profile, take a hard look at actual replacement costs in your area, and check with your lender before determining the right amount of coverage for you.

With that in mind, let’s explore the key components of a landlord insurance policy. Then we’ll show you how to inventory your insurance needs on a single spreadsheet to get accurate quotes with ease.

The Key Components of Landlord Insurance

Understanding what you’re actually buying helps you shop smarter. Here’s what the declarations page of a landlord insurance policy typically covers:

1. Dwelling Coverage (The Big One)

This is the “meat and potatoes” of the insurance policy. The dwelling coverage protects the physical structure and (typically) any attached structures as well. This is what dictates the size of the check you receive to repair or rebuild after fire, wind, hail, or other covered events.

The coverage amount is typically sized based on local replacement costs per square foot—not your property’s market value. In 2026, replacement costs are running 5-10+% higher than just a couple of years ago due to construction inflation.

2. Other Structures

Covers detached garages, sheds, fences, and other structures on the property. Usually sized around 10-20% of the total amount of dwelling coverage.

3. Landlord’s Personal Property

This bucket usually covers appliances you provide (refrigerators, washers, dryers, dishwashers, etc.), plus any tools or equipment (snowblowers, etc.) stored on site. It typically does NOT cover tenant belongings—that’s why smart landlords require tenants to carry renters insurance.

4. Loss of Rental Income

In the event of a major incident, you likely won’t be able to rent out your property while you complete repairs. This insurance provision reimburses lost rent (up to a point) while the property is uninhabitable due to a covered loss. You may want to size this coverage based on your actual monthly rent and realistic repair timelines in your market.

2026 reality check: Supply chain delays have improved, but skilled labor shortages persist. It may be wise to budget for 3-6 months of coverage, not 1-2, in the event of a major incident.

5. Liability Coverage

As you might expect, landlord liability coverage protects you from lawsuits when tenants or guests get injured at your property. Damage awards can be significant—this is probably not the place to “value engineer” cost savings.

Standard policies often include only $300K-$500K of coverage. Experienced investors carry $1M-$2M minimum, often with an umbrella policy on top.

6. Medical Payments

If someone is injured as a result of a condition present on your property, the medical payments coverage will usually kick in. Under this feature of your landlord policy, you won’t have to cover these costs out of pocket, up to a certain limit (usually $1,000-$5,000 per incident).

Deductibles (Sometimes) Influence Premiums

We’re generally big fans of relatively high deductibles. You’ll have to decide what “relatively” means for you. This is our standard preference because we’re usually loathe to file claims for smaller incidents. We can also reasonably afford to pay the deductibles when required. That might not be true for all rental property owners, so you’ll want to find your happy balance when it comes to landlord insurance deductibles.

It’s always best to ask your carrier or agent or broker to price out your policy premiums with a few different deductibles. That’s really the only way to accurately assess the risk/reward and make a fully informed decision about deductibles. You’ll notice that sometimes the premium responds nicely to a higher deductible, but other times you don’t save much at all and it’s best to keep it low.

Pay Attention to Exclusions (Where Carriers Hide Risk)

Most landlords don’t read the fine print until they file a claim and get denied. Standard exclusions in 2026 might include:

- Flood damage – May require separate NFIP or private flood policy

- Earthquake damage – Nearly always requires separate earthquake policy

- Hurricane/windstorm – Often excluded in coastal states; requires separate wind policy

- Mold – Usually capped at $10K-$25K unless caused by sudden covered peril

- Tenant damage – Intentional tenant destruction typically not covered

- Wear and tear – Normal aging, deferred maintenance, and gradual deterioration

It may not make any difference in the end, but it’s always best to know what you’re actually buying before you write the first premium check. We’ve found that when you ask up front for a list of policy exclusions, the whole process tends to go better. Either way, read the actual policy document to make sure you’re okay assuming all financial risks associated with the excluded scenarios. If not, consider getting a supplemental flood, earthquake, and/or hurricane policy to cover the gaps.

Smart move: When requesting quotes, specifically ask: “What major perils are excluded from this policy?” Then get supplemental coverage for any gaps you can’t afford to self-insure.

The Better Way: One Spreadsheet, Multiple Quotes

Here’s one way experienced landlords shop for insurance in 2026:

Step 1: Put all your property information into a single spreadsheet once

Step 2: Export a PDF and send it to multiple carriers simultaneously

Step 3: Get accurate quotes without answering 47 questions per carrier

Step 4: Compare apples-to-apples and make an informed decision

What Information Do Carriers Actually Need?

The exact personal and property information required differs among insurers. Virtually all will need the following:

- Your name, address, email, and phone number

- Insured property addresses

- Square footages of main buildings + detached structures

- Construction details like type, age, and condition

- Number of units by property

- Amount of dwelling coverage desired

- Amount of liability coverage desired

- Amount of income replacement coverage desired

- Property features like pool, roof material, security systems

- Claims history (usually 5 years)

Record this information all in one place. Update it whenever your portfolio changes. Never answer the same question twice!

Download the Free Landlord Insurance Spreadsheet

Save 3+ hours every time you shop for insurance.

Our Landlord Insurance Spreadsheet is a pre-formatted spreadsheet that helps you organize all your property details in one place. It includes:

✅ Property information template for up to 12 properties

✅ State-by-state carrier suggestions

✅ PDF export ready for sharing with agents

It’s used by savvy landlords to:

- Get accurate quotes from 3+ carriers in parallel

- Compare coverage options side-by-side

- Negotiate better rates with competing quotes

- Track annual renewals in one place

Join thousands of experienced landlords getting free tools, tax strategies, and market insights. Rent Bumper subscribers have ongoing access to all of our free resources, including the Landlord Insurance Spreadsheet.

It’s free to subscribe. Join now to receive your instant download link:

How to Use the Spreadsheet Effectively

Once you’ve filled out your personalized quote tracker, here’s how to maximize results:

Step 1: Build Your Carrier Shortlist

I’m often reminded that the insurance business is still a very regional industry. Even big national carriers don’t cover all geographies. Others have become very picky about localized risks from wildfires and coastal flooding. Of course, some major carriers don’t do landlord insurance at all.

Start with a phone call to screen carriers:

“Do you write landlord policies for [list your property types] in [your state/city]?”

This one question eliminates 60% of wasted effort. Many carriers don’t do landlord insurance at all. Others have pulled out of high-risk states entirely.

Major carriers writing landlord policies (as of 2026):

- State Farm

- Allstate

- Liberty Mutual

- Safeco

- USAA

- Travelers

- Foremost

- American Modern

- Progressive

- American Family

- Geico

- Steadily (landlord-specialist)

- Obie (landlord-specialist)

Regional variations matter: California? State Farm and Farmers have scaled back. Florida? Many national carriers exited; you might need surplus lines. Texas? Hailstorm claims have made some carriers very selective.

Step 2: Send Your Tracker PDF to 5-7 Carriers

Once you’ve confirmed they write landlord policies in your market, hide the column showing your existing premiums, export your portfolio summary to a new PDF file, and send it off with a simple email:

Subject: Landlord Insurance Quote Request – [# Properties] in [State]

Hi [Agent Name],

I’m getting quotes for landlord insurance on [#] rental properties in [City/State]. I’ve attached a complete property summary with all the information you’ll need.

Can you provide quotes for the coverage amounts listed? I’m comparing multiple carriers and intend to make a decision next week.

Thanks,

[Your Name]

Why this can work:

- They know you’re shopping around (motivates competitive pricing)

- You’ve done the legwork (makes their job easier)

- All information is consistent (enables accurate comparison)

- You set a deadline (creates urgency)

Step 3: Compare Apples to Apples

When quotes come back, verify:

- Same dwelling coverage amount (don’t compare $250K policy to $300K policy)

- Same deductible ($1,000 vs $2,500 can make a big difference)

- Same liability limits ($500K vs $1M isn’t apples-to-apples)

- Same loss of rent coverage (6 months vs 12 months)

- Equivalent exclusions (one policy might exclude more perils)

Watch for: The cheapest premium often comes with higher deductibles or lower coverage limits. Make sure you’re actually comparing equivalent protection.

Step 4: Negotiate & Decide

Once you have 3-5 solid quotes, you have leverage:

“Carrier X quoted me $1,450 for equivalent coverage. Can you match or beat that?”

Insurance is negotiable, especially when you’re bringing multiple properties or have a clean claims history. Don’t leave money on the table.

Final decision factors to consider beyond price:

- Claims reputation – Google “[carrier name] landlord insurance claims” to see how they actually handle losses

- Financial strength – Check AM Best rating (A- or better recommended)

- Local agent availability – Having a responsive local agent can be a plus when filing claims

- Payment flexibility – Monthly vs annual billing, autopay discounts

Special Considerations for 2026

High-Risk Markets Require Creative Solutions

If you own rentals in California, Florida, Texas, Louisiana, North Carolina, or a handful of other impacted states, standard market options may be limited or extremely expensive.

Alternatives:

- Surplus lines carriers – Non-admitted insurers that can write high-risk properties (usually 20-40% more expensive)

- State FAIR plans – Last-resort coverage (bare-bones protection, high premiums)

- Specialty landlord insurers – Services like Steadily and Obie that focus exclusively on helping you source competitive landlord coverage

Reality check: In some Florida zip codes, you might pay $4,000-$6,000/year for a single-family rental. Budget accordingly or reconsider those markets.

Short-Term Rentals Need Different Coverage

Running an Airbnb or VRBO short-term rental? Standard landlord policies typically won’t cover you. You need either:

- Short-term rental endorsement on your landlord policy

- Specialty STR insurance from carriers like Proper or CBIZ

- Commercial policy if you’re running full hospitality operations

We generally don’t recommend relying on Airbnb’s $1M Host Protection Insurance as your only coverage—it’s secondary and has significant gaps.

More reading: Avoid the Airbnb Host Insurance Trap

You’ll also find a few good tips regarding insuring your short term rental property buried in 99 Airbnb Tips for Expert Hosts.

Vacant Properties Cost More

Planning a major rehab with extended vacancy? Your standard policy might not cover it. Vacant property insurance runs 2-3x normal rates due to the increased risk of vandalism, theft, and undetected damage.

Options during rehabs:

- Short-term vacant property policy during renovation

- Builder’s risk insurance for major rehabs

- Keep existing policy and notify carrier (some allow 30-60 day vacancies)

The Annual Shopping Ritual

Insurance markets shift constantly. The carrier that gave you the best rate in 2024 might not be competitive in 2026. Here’s why:

- Carriers enter and exit markets based on loss ratios

- Rate increases vary wildly by zip code and property type

- Your claims history changes (or improves with no claims)

- New discounts become available (multi-policy, claims-free, etc.)

Best practice: Shop your insurance every single year at renewal, and at key moments in between if you have time. Even if you stick with the same carrier, having competing quotes can give you negotiating leverage for better rates.

Time investment with the spreadsheet: 2-3 hours annually

Potential savings: $100-$1,000+/year depending on portfolio size

Tax Deductibility

Landlord insurance premiums are 100% tax-deductible as a business operating expense. In 2026, that means:

- Federal tax benefit: 22-37% depending on your bracket

- State tax benefit: Varies by state (0-13.3%)

Example: $2,000 insurance premium in 24% federal bracket = $480 tax savings

Insurance premiums are usually tallied on Schedule E (Form 1040) under “Insurance” line item. Keep copies of your declarations pages and payment receipts in case of audit.

Avoid These Common Insurance Mistakes

Mistake #1: Homeowners insurance on a rental

Once tenants move in, your old homeowners policy is typically void. Claims may be denied. Get proper landlord coverage before the lease starts.

Mistake #2: Underinsured dwelling coverage

Replacement costs in 2026 are roughly 15-25+% higher than 2020 due to construction inflation. Review your coverage amounts annually. Being underinsured means eating the shortfall when disaster strikes.

Mistake #3: Skipping loss of rental income coverage

“I’ll just find new tenants quickly.” What if the property burns down and takes 6 months to rebuild? Lost rent can add up fast and your lender will expect you to keep the mortgage current regardless.

Mistake #4: Filing small claims

Insurance companies track claim frequency more than claim size. That $2,000 roof repair claim could cost you thousands in higher premiums for years. Consider self-insuring anything that comes in under your deductible plus 25%.

Mistake #5: Not reading exclusions

Assuming flood damage is covered (it’s often not included). Assuming mold is covered (usually capped at $10K-$25K). Assuming tenant damage is covered (often excluded). Read the policy and ask lots of questions early in the process.

Mistake #6: Letting policies auto-renew without shopping

Loyalty doesn’t pay in insurance. Carriers count on inertia. Shop annually or you’ll likely end up overpaying before too long.

The Bottom Line: System Beats Hustle

Landlord insurance is expensive and getting more expensive. In 2026, you might benefit from a system that:

- Organizes your property data once (no more answering the same questions 10 times)

- Gets you multiple competitive quotes (shopping can save $100-$1,000+/year)

- Ensures apples-to-apples comparisons (consistent data = accurate quotes)

- Makes annual shopping less painfull (update your tracker, send PDFs)

Download the spreadsheet, fill it out once, and let carriers compete for your business.